![The ultimate buyer’s guide for choosing the best TV [2023]](https://thenetick.co.ke/storage/2023/08/design-medium-360x180.jpg)

![5 Best AI Video Editor Tools [2023]](https://thenetick.co.ke/storage/2023/07/Featured-Image-360x180.png)

On Monday, trading platforms froze withdrawals, businesses lost employees, and anxious investors dumped their holdings, lowering the market cap of cryptocurrency to less than $1 trillion, down from $3 trillion in November.

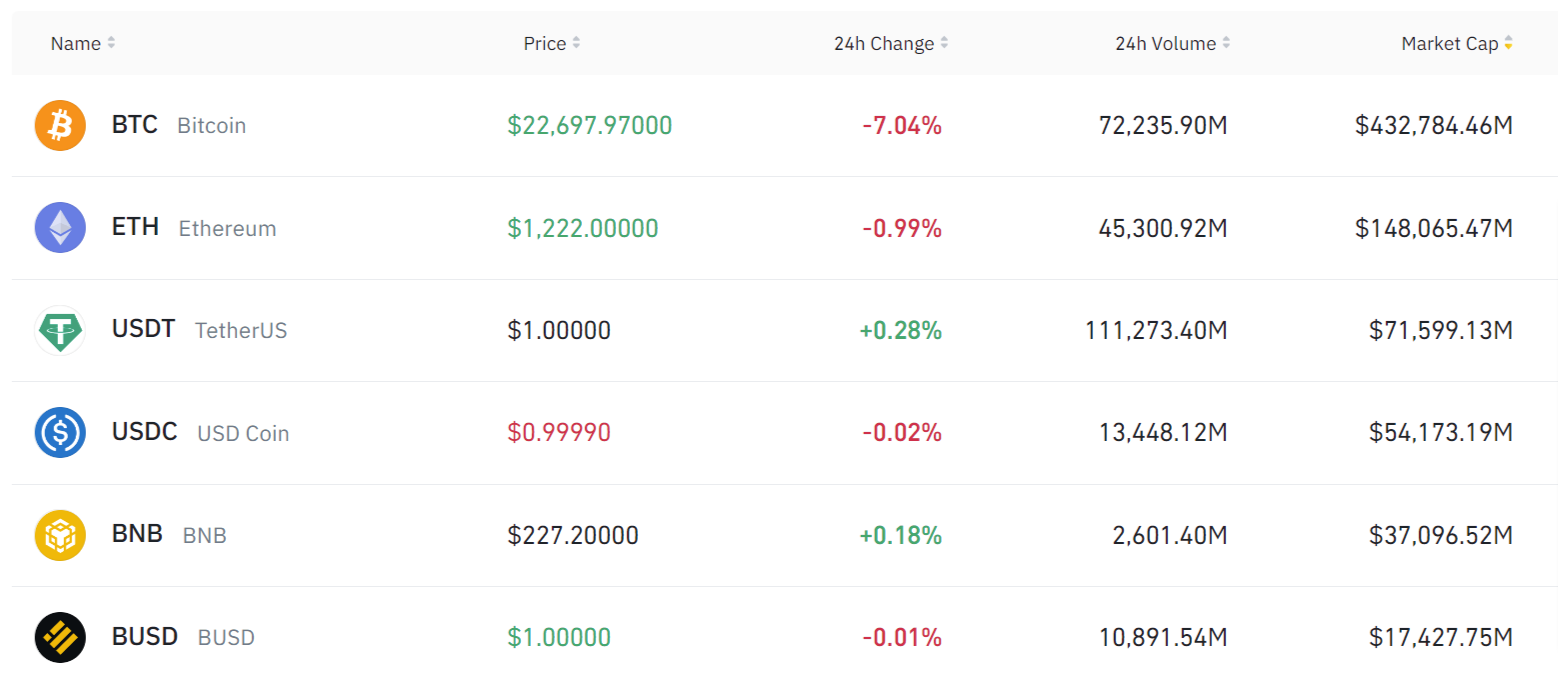

Bitcoin has dropped to an 18-month low, trading below $23,000. The most expensive cryptocurrency has dropped by 15% in the last 24 hours, while ethereum, the second most valued cryptocurrency, has dropped by 17%.

Due to macroeconomic challenges and rising interest rates, investors are exiting the riskiest assets. But it gets even worse. On Monday, the market demonstrated a fundamental distrust of cryptocurrencies and the infrastructure that enable them. What was already a severe slump began to resemble panic selling.

What’s happening?

Celsius, a major lender in the decentralized finance (defi) market, appears to have gone bankrupt. It’s unknown how bad things are for Celsius, but estimates range from $1.3 billion to $1.5 billion in crypto assets, including hundreds of millions in Ethereum and Bitcoin.

If the corporation is compelled to liquidate any of it, the price of the underlying assets will most certainly fall. And because some Celsius assets are staked somewhere, the price of certain crypto assets, such as stETH, which should ordinarily closely track the price of ordinary ETH, is under threat.

“Due to extreme market conditions, today we are announcing that Celsius is pausing all withdrawals, Swap, and transfers between accounts. We are taking this action today to put Celsius in a better position to honor, over time, its withdrawal obligations.” Celsius wrote in a blog post.

Celsius has effectively locked up its $12 billion in crypto assets under management, raising questions about the platform’s viability.

Coinbase shares fell 11% on Monday, reaching their lowest level since the company went public in April 2021.

Binance also took a break on Monday. For more than three hours, the world’s largest cryptocurrency exchange suspended bitcoin withdrawals “due to a stalled transaction producing a backlog.”

Lay-offs

BlockFi has joined a growing list of cryptocurrency companies that are lowering expenses by laying off employees.

On Monday, the platform announced a 20 percent reduction in headcount. Prior to the latest layoffs, the company had grown from 150 people at the end of 2020 to over 850.

Crypto.com reported a 260-person staff cut late last week. Gemini announced earlier this month that it would be laying off 10% of its personnel and warned that the industry is in a “contraction phase” known as “crypto winter.”

Meanwhile, cryptocurrency company, Coinbase has announced a hiring freeze for the “foreseeable future” and expects to cancel certain job offers.

Despite the volatility and recent price drop, many experts believe Bitcoin is on its way to crossing the $100,000 barrier, albeit they differ on when that will happen. In addition, according to a recent Deutsche Bank study, over a fifth of Bitcoin investors think Bitcoin prices would exceed $110,000 in five years.

Is it time to buy the dip or is it the beginning of an end?

{kind=link}